TL;DR: The SAR narrative is the single most valuable element for law enforcement, yet most narratives lack the specificity investigators need to act. FinCEN's October 2025 guidance shifted expectations from volume to quality, and institutions filing over 4.1 million SARs annually now face pressure to make every narrative count. A stronger narrative answers who, what, when, where, why, and how — with enough transactional detail and context that an investigator can assess merit without requesting additional information.

What the Narrative Actually Does

The SAR narrative is the only free-text field on the entire filing. Everything else — subject information, transaction dates, filing institution details — lives in structured checkboxes and dropdown fields. The narrative is where an analyst explains what happened, why it looked suspicious, and what the institution did about it.

Law enforcement treats the narrative as the starting point for case assessment. According to Forvis Mazars' 2026 analysis, IRS Criminal Investigation searched BSA data in 94% of its cases, with nearly 80% of investigations involving subjects associated with SARs. When IRS-CI utilized BSA filings in 2025, it achieved a 98% conviction rate and secured more than $450 million in asset forfeitures. The narrative is what connects a filing to an actual investigation — or buries it in a stack of unusable reports.

This matters because the filing volume is enormous. In 2025, financial institutions submitted more than 4.1 million SARs — a 7.99% increase over 2024 — bringing the cumulative total past 47 million since the SAR's creation. With that volume, a vague or boilerplate narrative disappears. A specific, well-structured one gets read.

Why Most Narratives Fall Short

Compliance teams often write SAR narratives defensively — proving that the institution met its filing obligation rather than equipping law enforcement with actionable intelligence. The result is narratives that check boxes without telling a story.

Three patterns drive most quality failures. First, analysts aggregate transaction data into summary ranges rather than itemizing individual dates, amounts, and counterparties. A narrative stating "the subject conducted multiple transactions totaling approximately $85,000 over a three-month period" gives an investigator almost nothing to work with. Second, narratives frequently omit the source of funds, the destination, or the beneficiary — the flow-of-funds detail that FFIEC's Appendix L on SAR quality calls essential. Third, many narratives skip the "why" — what made this activity suspicious relative to the customer's known profile and expected behavior.

FinCEN's October 2025 FAQ reinforced this point by shifting guidance from volume-driven filing to quality-focused reporting. The expectation of filing continuing SARs on a rigid 120-day calendar is gone. Instead, institutions should use risk-based monitoring to identify and report new suspicious activity as it occurs, with each narrative documenting what the monitoring controls actually surfaced rather than recycling prior language on a schedule.

The Five W's and How to Use Them

Every SAR narrative should answer six questions: who, what, when, where, why, and how. FinCEN's SAR Narrative Guidance Package establishes these as the essential elements, but most analysts treat them as a loose checklist rather than a structural framework.

Who

Identify every subject by full name, role, and relationship to the account. If the activity involves multiple parties — a business owner, a signatory, and a beneficiary — name each one and explain their involvement. Pronouns without clear antecedents force investigators to re-read.

What

Describe the specific transactions and activity patterns that triggered the alert. Use individual dates and dollar amounts rather than aggregated ranges. A narrative listing "12 cash deposits between March 3 and March 28, 2025, ranging from $8,200 to $9,800, totaling $107,400" is materially more useful than "multiple cash deposits below the CTR threshold."

When

Establish the timeline. Note when the suspicious activity was first identified, the duration of the pattern, and any relevant date clusters. If the institution has filed prior SARs on this subject, reference those filings and explain what changed.

Where

Include the branch locations, jurisdictions, and geographic patterns involved. Cross-border transactions, multiple branch deposits, and geographic inconsistencies with the customer's profile all warrant explicit mention.

Why

This is where most narratives fail. Explain what made the activity suspicious — not just that it triggered a rule, but why it deviates from the customer's expected behavior. A retail business owner making structured cash deposits is suspicious because the business type does not generate cash revenue, not simply because the deposits fell below $10,000.

How

Describe the method of operation. How did the subject move funds? What mechanisms, accounts, or intermediaries were used? If the activity follows a known typology — structuring, funnel accounts, rapid movement of funds — name it explicitly. FinCEN has requested that institutions include specific key terms such as "human trafficking," "funnel account," or "political corruption" where applicable, because these terms allow law enforcement to search and surface relevant filings efficiently.

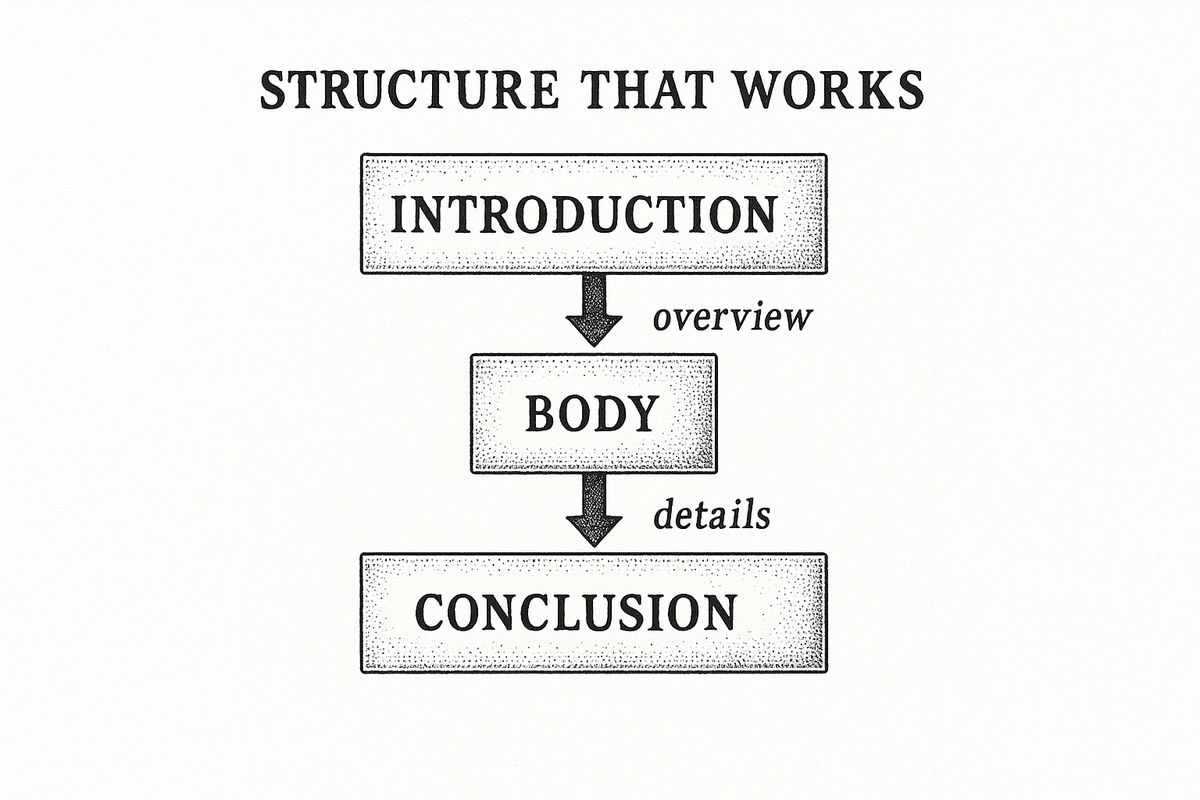

Structure That Works

The most effective SAR narratives follow an introduction-body-conclusion format — the same structure as any clear analytical writing.

The introduction provides a concise overview: who the subject is, what type of activity is being reported, and the aggregate dollar amount. This section orients the reader. FinCEN reviewers and law enforcement analysts process large volumes of filings, and a clear opening determines whether the narrative gets a full read or a skim.

The body presents the detailed chronology. Walk through the transactions in order, connecting each step to the next. This is where flow-of-funds analysis belongs — where the money came from, how it moved, and where it ended up. Include account numbers, transaction dates, dollar amounts, and counterparties. If the institution took any action — restricting the account, contacting the customer, filing a prior SAR — document it here.

The conclusion states the institution's assessment: what makes this activity suspicious, what typology it maps to, and whether the institution has taken or plans to take any remedial action. This is not a hedge. State the suspicion directly.

One detail that separates strong narratives from adequate ones: referencing prior filings. If the institution has filed previous SARs on the same subject, cite the prior BSA identifiers and explain what new activity prompted the current filing. Continuing SAR narratives should document that monitoring controls identified new behavior, not simply restate the original narrative with updated dates.

Common Mistakes and How to Fix Them

Boilerplate language is the most frequent problem. Phrases like "the activity is inconsistent with the customer's known profile" appear in thousands of narratives without specifying what the customer's profile actually looks like or how the activity deviates from it. Replace generic characterizations with specific comparisons: expected monthly deposit volume versus actual volume, stated business type versus observed transaction patterns.

Overreliance on aggregated data ranks second. When analysts report total amounts and date ranges instead of individual transactions, they strip out the patterns that make activity suspicious. Structuring, for instance, only becomes visible when individual deposit amounts are listed — a summary total obscures the very behavior being reported.

Passive voice and hedge language weaken otherwise solid narratives. "It was determined that the activity may potentially be inconsistent with expectations" communicates nothing an investigator can act on. "The subject deposited $9,500 in cash on four consecutive business days at different branches, which is inconsistent with the stated business type of online consulting" gives the investigator a clear thread to pull.

Missing disposition information is another gap. The narrative should state what the institution did in response — account restrictions, relationship termination, enhanced monitoring — not just what the subject did. Examiners look for evidence that the compliance program drove an outcome, not just a filing.

What Changes with FinCEN's October 2025 Guidance

FinCEN's October 2025 FAQ marked a meaningful shift in SAR expectations. Two changes matter most for narrative quality.

First, the threshold clarification. A transaction at or near the $10,000 CTR threshold does not automatically trigger a SAR obligation. The institution must have awareness, suspicion, or reason to believe the transaction was structured to avoid reporting. This means the narrative needs to explain the basis for suspicion — not simply cite proximity to a threshold as evidence.

Second, the continuing SAR change. The rigid 120-day filing cycle is no longer the standard. Institutions can file continuing SARs based on risk-based monitoring rather than calendar-driven schedules. This places more weight on each narrative to demonstrate what new activity the monitoring program surfaced. A continuing SAR that rehashes old language without identifying new conduct signals to examiners that the monitoring program may not be functioning as intended.

Both changes push in the same direction: narratives that demonstrate analytical judgment, not reflexive filing. Institutions that build auditable reasoning into their compliance workflows are better positioned to produce narratives that satisfy this standard.

Where Sphinx Fits

Sphinx's Auto-SAR capability automates the evidence-gathering, chronology-building, and narrative-drafting stages of SAR preparation. The system pulls transaction data, customer profile information, and prior filing history into a structured draft that follows FinCEN's five-W framework. Every element of the draft — the data sources consulted, the logic applied, and the language generated — is logged in an auditable decision trail that compliance teams can review, edit, and approve before submission. The goal is not to remove human judgment from SAR filing but to ensure that analysts spend their time on analysis rather than data assembly. For institutions that need additional investigative capacity, reducing review time per case compounds across thousands of filings annually.

Frequently Asked Questions

What are the five essential elements of a SAR narrative?

A SAR narrative must answer who is involved, what suspicious activity occurred, when it happened, where the activity took place, and why it is suspicious. FinCEN also recommends including the method of operation — how the subject conducted the activity. Each element should include specific details rather than generalized descriptions.

How long should a SAR narrative be?

There is no prescribed length. A narrative should be as long as necessary to convey the full scope of suspicious activity with specific transaction details, timelines, and supporting context. A concise narrative with granular detail is more valuable than a lengthy one padded with boilerplate language. The FinCEN SAR form provides a free-text field that accommodates extended narratives when the activity warrants it.

Did FinCEN change SAR filing requirements in 2025?

Yes. FinCEN's October 2025 FAQ clarified that the 120-day continuing SAR cycle is no longer mandatory. Institutions can now file continuing SARs based on risk-based monitoring rather than a fixed calendar. The guidance also clarified that transactions near the $10,000 CTR threshold do not automatically require a SAR — institutions need a reasonable basis for suspicion beyond threshold proximity.

What keywords should be included in a SAR narrative?

FinCEN maintains a consolidated list of SAR narrative key terms — including "human trafficking," "funnel account," "structuring," "political corruption," and others — that help law enforcement search and surface relevant filings. Including applicable key terms in the narrative improves the filing's discoverability and investigative utility.

Can technology help improve SAR narrative quality?

Automated tools can accelerate the data-gathering and drafting stages of SAR preparation by pulling transaction records, customer profiles, and prior filing history into structured narrative frameworks. The compliance analyst still reviews, edits, and approves the final narrative. Automation reduces the risk of missing key details and frees analyst time for the analytical judgment that makes narratives useful to law enforcement.

.png)