TL;DR: Compliance software for financial services has split into distinct categories: AML screening specialists, identity orchestration platforms, KYB verification tools, security compliance automation, and agentic AI systems that execute compliance workflows end to end. According to Grand View Research, the global compliance software market reached $35.82 billion in 2025 and is projected to grow at a 10.5% CAGR through 2033. This guide ranks the leading platforms, explains what separates them, and provides a framework for choosing the right one.

What Compliance Software Covers in Financial Services

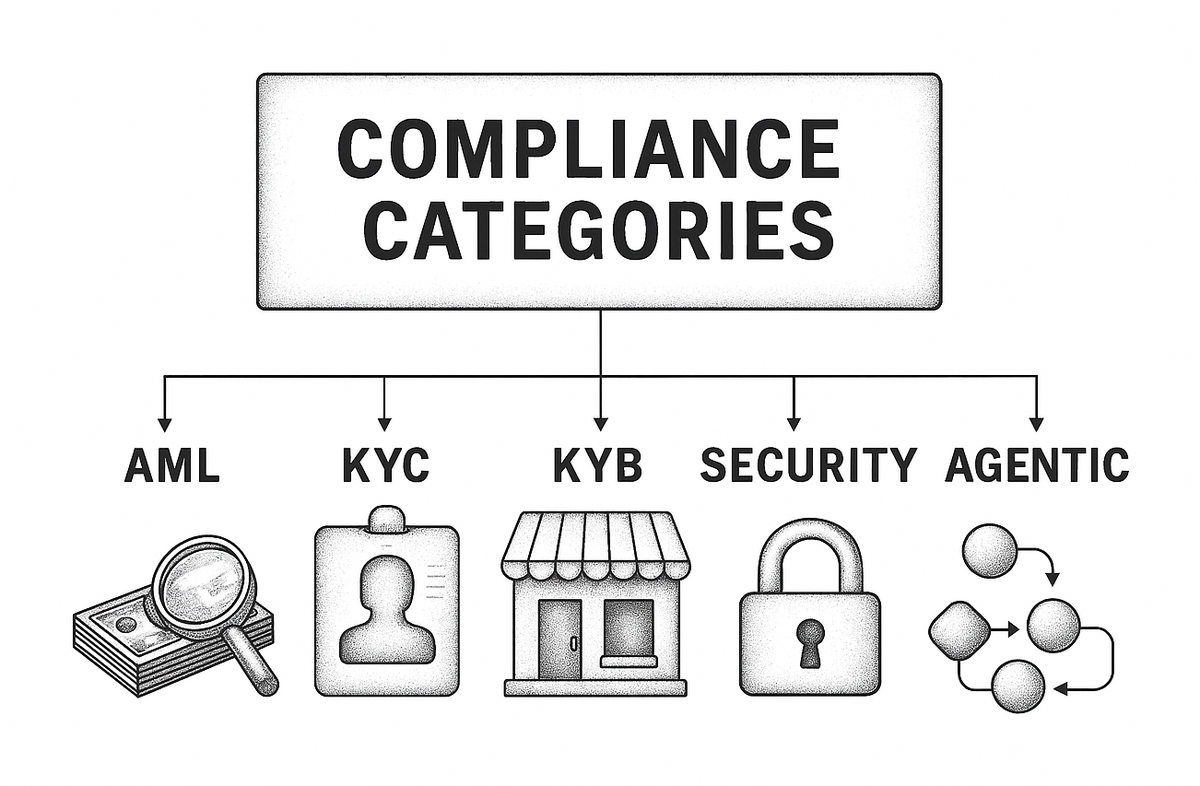

Compliance software automates the regulatory obligations that financial institutions must meet to operate. The category spans a wide range of functions: screening customers against sanctions and PEP lists, monitoring transactions for suspicious activity, verifying business identities during onboarding, managing audit trails, and filing regulatory reports. No single platform covers all of these equally well, which is why most compliance teams run a stack of two or three tools rather than relying on one vendor.

The market has segmented along functional lines. Some vendors specialize in AML screening and transaction monitoring. Others focus on identity verification and KYC orchestration. A newer cohort targets KYB verification, addressing the distinct challenge of validating business entities, beneficial owners, and corporate structures. Security compliance platforms like Vanta and Drata handle SOC 2, ISO 27001, and similar frameworks that overlap with but differ from financial crime compliance. And agentic AI platforms have emerged to handle the operational work itself, triaging alerts and resolving cases rather than just flagging them.

The distinction matters for buyers. A fintech scaling its customer onboarding has different needs than a bank rebuilding its transaction monitoring program or a payments company preparing for a regulatory examination.

Why Compliance Software Matters More in 2026

Three shifts are forcing financial institutions to re-evaluate their compliance technology.

Regulatory frameworks are tightening around effectiveness

In April 2026, FinCEN proposed a rule to fundamentally reform AML/CFT programs under the Bank Secrecy Act. The proposed rule refocuses compliance obligations on effectiveness, distinguishing between deficiencies in program design versus implementation. The UK followed suit with the Money Laundering and Terrorist Financing (Amendment) Regulations 2026, expanding enhanced due diligence requirements for cryptoasset businesses and aligning with updated FATF recommendations. For compliance teams, the message from both sides of the Atlantic is the same: regulators want measurable outcomes, not just documented procedures.

The cost of non-compliance keeps climbing

Financial institutions paid over $4 billion in AML non-compliance penalties globally in 2025, according to data compiled by Sanctions Lookup. The US accounted for roughly $1.97 billion of that total. FinCEN assessed a record $80 million penalty against a single broker-dealer for BSA violations tied to CDD failures that allowed high-risk customers, including individuals with reported ties to illicit actors, to access the US financial system without appropriate controls. Non-compliance now costs 2.71 times more than compliance when factoring in business disruption, revenue loss, and productivity impact alongside direct fines.

Compliance spending is rising, not falling

According to LexisNexis Risk Solutions, the total cost of financial crime compliance in the US and Canada reached $61 billion, with 99% of financial institutions reporting cost increases. Half of compliance leaders surveyed by ProSight Financial Association expect budgets to rise 5% or more annually over the next several years. The pressure is coming from both sides: regulations are expanding, and the volume of alerts, customers, and transactions continues to grow. Software that reduces manual effort per case directly impacts the operating budget.

How to Evaluate Compliance Software

TL;DR:

Evaluating compliance software starts with matching the tool to the function, assessing integration depth, and measuring false positive impact.

Choosing the right compliance platform starts with understanding where the operational burden sits. A feature comparison spreadsheet misses the point. What matters is whether the software addresses the specific bottleneck in your compliance program.

Match the tool to the function

Compliance software is not interchangeable. A platform built for sanctions screening will not solve a transaction monitoring backlog. A KYB verification tool will not help with SOC 2 readiness. Before evaluating vendors, map your compliance obligations to the functions you need automated: screening, monitoring, onboarding, case management, reporting, or audit readiness. Then shortlist vendors that specialize in those areas.

Assess integration depth

Most financial institutions already run core banking systems, payment processors, and CRM platforms. The compliance tool needs to work within that stack. Evaluate API coverage, data source integrations, and whether the platform requires rip-and-replace or can layer on top of existing infrastructure. Vendors that aggregate data from multiple sources into a single decisioning layer, like Alloy with its 190+ integrations, reduce the integration tax significantly.

Measure false positive impact

For teams dealing with AML screening and monitoring, false positive rates remain the defining operational metric. A platform that screens accurately but generates thousands of non-actionable alerts per day creates more work than it saves. Evaluate how the vendor handles match scoring, alert prioritization, and the operational cost per resolved case.

Verify regulatory coverage

Financial services compliance spans multiple regimes: BSA/AML, OFAC sanctions, FATF recommendations, EU AMLDs, FCA requirements, and increasingly MiCA for crypto. A platform strong in US regulatory reporting may have gaps in European or APAC jurisdictions. Match the vendor's regulatory coverage to where you operate and where you plan to expand.

Best Compliance Software for Financial Services

The following platforms represent the leading options across different compliance functions. Each evaluation covers core capabilities, strengths, limitations, and ideal fit. Rankings reflect a combination of market presence, technology differentiation, and suitability for modern compliance operations.

1. ComplyAdvantage

ComplyAdvantage built its position on proprietary risk data. The platform aggregates information from thousands of structured and unstructured sources to create a real-time risk database covering sanctions, PEP exposure, and adverse media. It handles customer screening, transaction monitoring, and case management through a single API-first SaaS interface. Goldman Sachs led its $70 million Series D, and disclosed customers include Affirm, Coinbase, and Allianz.

Strengths: Real-time data refresh cycles give ComplyAdvantage an edge on adverse media detection through NLP. Configurable search profiles let teams fine-tune screening sensitivity without vendor involvement. The API-first architecture integrates cleanly with modern tech stacks. ComplyLaunch offers a startup-friendly entry tier.

Limitations: Transaction monitoring capabilities are less mature than the screening product. Complex investigation workflows lack the depth of enterprise-grade platforms. Limited suitability as a standalone solution for Tier 1 banks processing billions of daily transactions.

Best fit: Mid-market fintechs, neobanks, and payment companies that prioritize screening data quality and fast API integration.

2. NICE Actimize

NICE Actimize remains the default compliance platform for the world's largest banks. Its full-stack offering covers AML, fraud, market abuse, and communication surveillance. The platform processes billions of transactions daily across a client base that includes most top-50 global banks. The SAM and X-Sight products span the entire financial crime lifecycle from CDD through SAR filing.

Strengths: Two decades of enterprise deployment experience. Comprehensive scenario libraries for transaction monitoring. Deep integration with core banking systems from Temenos, FIS, and Fiserv. Regulatory reporting templates covering FinCEN, FCA, MAS, and dozens of other jurisdictions.

Limitations: Implementation timelines stretch to 12-18 months for full deployments. The platform carries technical debt from acquisitions and legacy architecture. Innovation pace lags newer competitors on AI-native capabilities. Enterprise pricing puts it out of reach for most mid-market buyers.

Best fit: Tier 1 and Tier 2 banks with complex multi-jurisdictional requirements and dedicated compliance technology teams.

3. Vanta

Vanta focuses on security compliance automation rather than financial crime. The platform automates evidence collection and continuous monitoring for SOC 2, ISO 27001, HIPAA, PCI DSS, and GDPR. For financial services firms, Vanta addresses the security and operational risk side of compliance, particularly relevant for fintechs that need to demonstrate security posture to banking partners and regulators.

Strengths: Automates up to 90% of the evidence collection work for security compliance audits. Continuous monitoring flags control failures in real time rather than waiting for annual audit cycles. Integrates with 300+ tools across cloud infrastructure, identity management, and endpoint security. Strong fit for fintechs navigating SOC 2 requirements for the first time.

Limitations: Does not cover financial crime compliance: no AML screening, transaction monitoring, or KYC verification. Focused on security frameworks rather than BSA/AML or OFAC obligations. Financial services firms will need separate tools for financial crime compliance alongside Vanta.

Best fit: Fintechs and financial services firms that need to achieve and maintain SOC 2, ISO 27001, or PCI DSS certification alongside their financial crime compliance stack.

4. Alloy

Alloy positions itself as an identity decisioning platform. It orchestrates data from 190+ sources, including credit bureaus, government databases, and watchlists, into automated decisioning workflows for onboarding, transaction monitoring, and ongoing due diligence. The platform serves as an integration layer that sits between data providers and compliance decisions.

Strengths: Flexible workflow builder allows compliance teams to create and modify decisioning rules without engineering support. Aggregates data from 190+ sources into a single orchestration layer. Strong KYC and KYB capabilities alongside AML screening. The no-code interface accelerates time to value.

Limitations: Transaction monitoring is less sophisticated than purpose-built AML platforms. The platform excels at onboarding and identity verification but has thinner capabilities for ongoing monitoring and SAR filing. Best suited to US-centric operations with more limited global coverage.

Best fit: US-based fintechs and banks that want to unify identity verification, KYC, and AML screening in a single orchestration layer.

5. Middesk

Middesk specializes in business identity verification. The platform verifies business registration, beneficial ownership, tax identification, and screens businesses against sanctions and watchlists. For financial institutions onboarding business customers, Middesk addresses the KYB gap that most KYC-focused platforms leave open.

Strengths: Purpose-built for business verification with direct access to Secretary of State databases, IRS records, and other primary sources. Automated UBO identification and verification. Self-serve onboarding makes it accessible to growth-stage companies. Strong fraud detection signals specific to business entities.

Limitations: Not designed for individual KYC or transaction monitoring. Functions as a complement to a full compliance platform rather than a replacement. Limited international coverage compared to global KYB solutions. Does not cover ongoing monitoring or case management.

Best fit: Fintechs and banks that onboard business customers and need robust, automated KYB verification to complement their existing KYC and AML tools.

6. Sumsub

Sumsub provides a global identity verification and compliance platform covering KYC, KYB, AML screening, and transaction monitoring. The platform supports document verification, biometric checks, and address verification across 220+ countries. Sumsub also offers travel rule compliance for crypto businesses, positioning it for both traditional financial services and digital asset companies.

Strengths: Broad geographic coverage with document verification support across 14,000+ document types. Integrated sanctions screening, PEP checks, and adverse media monitoring. Liveness detection and deepfake prevention for identity verification. Built-in travel rule compliance for VASPs.

Limitations: AML screening data depth is thinner than dedicated screening platforms like ComplyAdvantage. Transaction monitoring capabilities are newer and less battle-tested at enterprise scale. The breadth of features means less depth in any single compliance function compared to specialists.

Best fit: Companies operating across multiple jurisdictions that need a single platform for identity verification, basic AML screening, and crypto compliance.

7. Drata

Drata, like Vanta, automates security and compliance frameworks. The platform covers SOC 2, ISO 27001, HIPAA, PCI DSS, GDPR, and newer frameworks including NYDFS Part 500, making it directly relevant to financial services firms. Drata holds a 4.8/5 G2 rating and has expanded its regulatory coverage to address fintech-specific requirements.

Strengths: Automated evidence collection and continuous monitoring across compliance frameworks. Strong coverage of NYDFS Part 500, which applies directly to financial services firms operating in New York. Third-party risk management capabilities for vendor diligence. Accessible pricing starting around $500/month makes it viable for growth-stage fintechs.

Limitations: Same category distinction as Vanta: Drata handles security compliance, not financial crime compliance. No AML, KYC, or sanctions screening capabilities. Financial institutions need separate tooling for BSA/AML obligations.

Best fit: Fintechs racing toward NYDFS Part 500, SOC 2, or ISO 27001 certification on a mid-market budget.

| Platform | Primary Function | Best For | AML/KYC Coverage | Deployment |

|---|---|---|---|---|

| ComplyAdvantage | AML screening + risk data | Mid-market fintechs | Strong screening, growing TM | SaaS |

| NICE Actimize | Full financial crime lifecycle | Tier 1-2 banks | Comprehensive | On-prem / Cloud |

| Vanta | Security compliance | Fintechs needing SOC 2/ISO | None | SaaS |

| Alloy | Identity decisioning | US fintechs + banks | Strong KYC, moderate AML | SaaS |

| Middesk | KYB verification | Business onboarding teams | KYB only | SaaS |

| Sumsub | Global identity + AML | Multi-jurisdiction firms | Broad but less deep | SaaS |

| Drata | Security compliance | Fintechs needing NYDFS/SOC 2 | None | SaaS |

| Sphinx | Agentic compliance ops | Alert-heavy teams | AML triage + case resolution | SaaS |

Where Sphinx Fits

The platforms above address different compliance functions: screening, monitoring, onboarding, security frameworks, and business verification. Sphinx addresses a different bottleneck: the operational work of resolving compliance cases.

Sphinx deploys AI agents that triage alerts, review cases, and document decisions using the same tools and workflows that human analysts follow. The agents log into existing compliance platforms, pull the relevant data, apply the institution's policies, and produce audit-ready documentation for every decision. Equals Money automated 87.3% of compliance reviews after deploying Sphinx, clearing a six-month alert backlog in two days. Across its customer base, Sphinx reduces case review time by 80% and resolves 98% of cases same-day.

Sphinx does not replace screening engines, transaction monitoring systems, or security compliance platforms. It works alongside them, handling the high-volume, repetitive case work that consumes analyst time. For compliance teams running ComplyAdvantage, NICE Actimize, or any of the platforms listed above, Sphinx layers on top to resolve the alerts those systems generate. Teams interested in how this applies to managed compliance operations can explore Sphinx Frontline, which combines AI agents with human oversight for institutions that need both technology and capacity.

Frequently Asked Questions

What is compliance software for financial services?

Compliance software for financial services automates the regulatory obligations that banks, fintechs, and payment companies must meet. This includes AML screening, transaction monitoring, KYC/KYB verification, sanctions checks, case management, and regulatory reporting. Most financial institutions use multiple compliance tools rather than a single platform, since the category spans distinct functions with different technical requirements.

How much does compliance software cost?

Costs vary widely by vendor and scope. Entry-level SaaS platforms like ComplyAdvantage start around $99 per month. Security compliance tools like Drata begin at roughly $500 per month. Enterprise platforms like NICE Actimize and MetricStream run $400,000 or more annually. According to community banking data, the typical US bank spends between $318,000 and $763,000 annually on compliance, representing 5-12% of non-interest expenses.

What is the difference between compliance software and GRC software?

GRC (governance, risk, and compliance) software takes a broader view, covering enterprise risk management, policy management, and internal audit alongside compliance. Compliance software for financial services focuses specifically on regulatory obligations like AML, KYC, and sanctions screening. Some vendors, such as MetricStream and OneTrust, straddle both categories. Financial institutions typically need dedicated compliance tools for financial crime alongside broader GRC platforms for enterprise governance.

Can one platform handle all financial services compliance needs?

No single platform covers every compliance requirement. AML screening, transaction monitoring, KYB verification, and security compliance (SOC 2, ISO 27001) each require specialized capabilities. Most compliance teams run a stack of two to four tools. The key decision is which functions to consolidate under one vendor and where to use best-of-breed specialists. Orchestration platforms like Alloy can reduce the integration complexity of a multi-vendor stack.

How is AI changing compliance software in 2026?

AI is shifting compliance software from detection to resolution. Earlier generations added machine learning to improve screening accuracy or reduce false positives in transaction monitoring. The current wave applies AI agents that execute compliance workflows autonomously: triaging alerts, reviewing cases, and filing reports. FinCEN's 2026 proposed rule, which emphasizes program effectiveness over procedural volume, aligns with this shift. Platforms that reduce the cost per resolved case, rather than just the number of alerts generated, are gaining traction.

.png)