TL;DR: The best AML software in 2026 combines real-time transaction monitoring, sanctions screening, and AI-driven alert triage to cut false positives and accelerate investigations. With false positive rates still hitting 85-95% across the industry, the platforms that win are the ones that surface genuine risk instead of burying analysts in noise. This guide ranks the leading AML platforms, explains what separates them, and offers a framework for choosing the right one.

What AML Software Actually Does

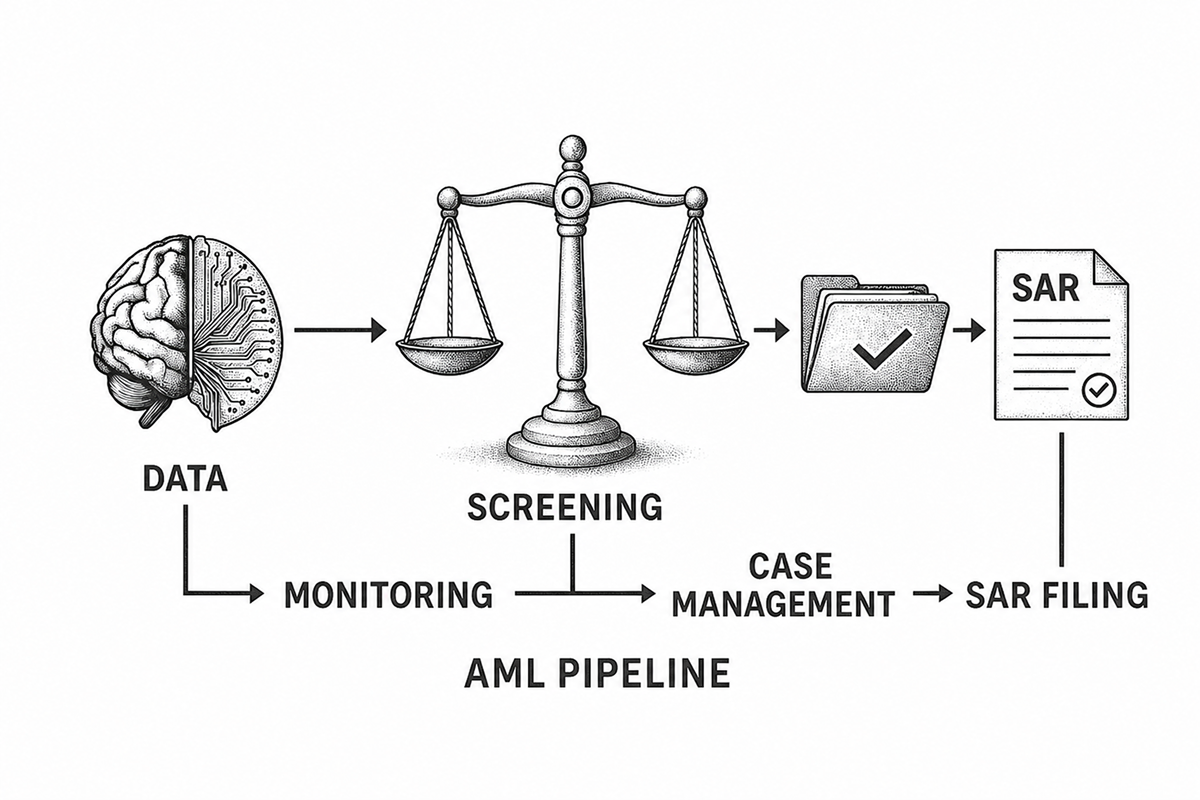

AML software detects, investigates, and reports financial crime. It sits between raw transaction data and regulatory obligations, automating the work that compliance teams would otherwise do manually: screening customers against sanctions and PEP lists, monitoring transactions for suspicious patterns, managing cases through investigation, and filing SARs when warranted.

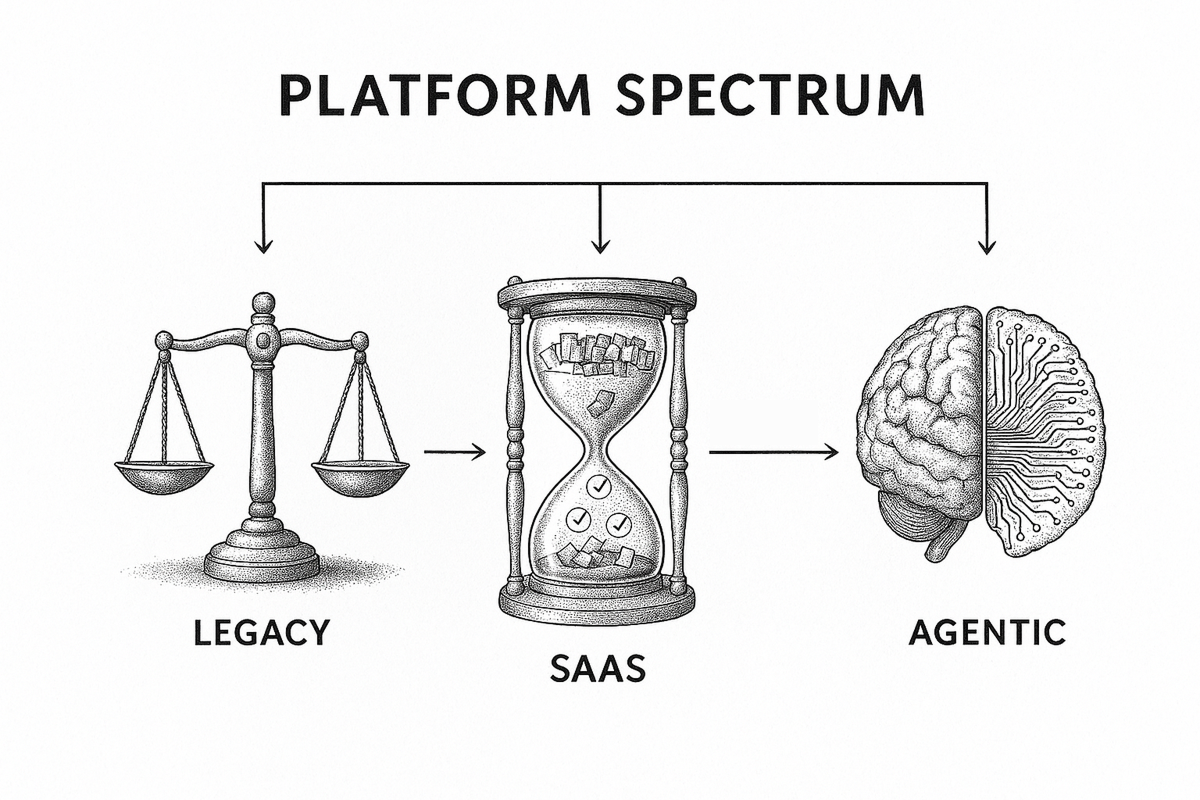

The category has split into distinct segments. Legacy enterprise stacks from vendors like NICE Actimize and SAS serve Tier 1 banks with deep integration requirements. Modern SaaS platforms like ComplyAdvantage and Alloy target mid-market fintechs and neobanks that need faster deployment. Blockchain analytics specialists like TRM Labs focus on crypto-native risks. And a newer wave of agentic platforms, including Sphinx, apply autonomous AI agents to compliance workflows rather than just adding ML models on top of rules engines.

What matters is not which segment a vendor falls into, but whether the software actually reduces the operational burden on compliance teams while maintaining regulatory defensibility.

What Is Driving AML Software Adoption in 2026

Three forces are reshaping how financial institutions buy and deploy AML technology.

Regulatory pressure is shifting toward effectiveness

In April 2026, FinCEN proposed a rule to fundamentally reform AML/CFT programs under the Bank Secrecy Act. The core shift: regulators now want to measure programs by their ability to stop illicit finance, not by the volume of paperwork they produce. Treasury Secretary Scott Bessent framed it directly, stating the proposal "restores common sense with a focus on keeping bad actors out of the financial system, not burying America's banks in more red tape." The UK followed a similar path with its Money Laundering and Terrorist Financing (Amendment) Regulations 2026, tightening crypto due diligence requirements and aligning with updated FATF standards ahead of the UK's mutual evaluation later this year.

False positives remain the central operational problem

According to Facctum's State of AML Compliance 2026 report, false positive rates across screening and monitoring systems still range between 85% and 95%. Compliance teams spend up to 90% of their time investigating alerts that lead nowhere. A large institution processing 10,000 alerts per day at a 90% false positive rate generates 9,000 non-actionable alerts daily, consuming roughly 4,500 analyst hours. That is not a detection problem. It is an efficiency crisis. Platforms that genuinely reduce false positives deliver measurable ROI by freeing analysts to focus on real threats.

The market is growing fast

The global AML software market reached $3.22 billion in 2025 and is projected to hit $3.75 billion in 2026, growing at a 15.9% CAGR through 2030 according to data compiled by CoinLaw from The Business Research Company. AI-specific AML spending is on pace to reach $15.38 billion by 2035. The money is following the problem: 62% of institutions already use AI or ML for AML monitoring, and adoption is expected to reach 90%.

Best AML Software in 2026

The following platforms represent the leading options across different buyer segments. Each evaluation covers core capabilities, strengths, limitations, and ideal fit. Rankings reflect a combination of market presence, technology differentiation, and suitability for modern compliance operations.

1. ComplyAdvantage

ComplyAdvantage built its reputation on proprietary risk data. Rather than relying solely on traditional watchlists, it aggregates information from thousands of structured and unstructured sources to create a real-time risk database covering sanctions, PEP exposure, and adverse media. The platform handles customer screening, transaction monitoring, and case management through a single SaaS interface.

Strengths: Real-time data refresh cycles give ComplyAdvantage an edge on adverse media detection. The API-first architecture integrates cleanly with modern tech stacks. Configurable search profiles let teams fine-tune screening sensitivity without vendor involvement. Pricing starts at $99 per month for smaller operations, making it accessible to mid-market buyers.

Limitations: Transaction monitoring capabilities, while improving, are less mature than the screening product. Larger institutions with complex multi-entity structures may find the case management workflows insufficient compared to enterprise-grade alternatives. Limited support for blockchain-native transaction types.

Best fit: Mid-market fintechs, payment companies, and neobanks that prioritize data quality and fast integration over legacy system compatibility.

2. NICE Actimize

NICE Actimize remains the default choice for Tier 1 banks. Its SAM (Suspicious Activity Monitoring) and X-Sight platforms cover the full AML lifecycle: customer due diligence, transaction monitoring, sanctions screening, and regulatory reporting. The platform processes billions of transactions daily across its global client base.

Strengths: Deep domain expertise built over two decades of enterprise deployments. Comprehensive scenario libraries for transaction monitoring. Strong integration with core banking systems from Temenos, FIS, and Fiserv. Extensive regulatory reporting templates covering FinCEN, FCA, MAS, and other jurisdictions. Holds roughly 17% global AML software market share.

Limitations: Implementation timelines stretch to 12-18 months for full deployments. The platform carries significant technical debt from acquisitions and legacy architecture. Innovation pace lags newer competitors, particularly on AI-native alert triage. Enterprise pricing places it out of reach for most mid-market buyers.

Best fit: Tier 1 and Tier 2 banks with complex multi-jurisdictional requirements and dedicated compliance technology teams.

3. LexisNexis Risk Solutions

LexisNexis competes primarily on data breadth. Bridger Insight XG handles sanctions and PEP screening, while the broader Risk Solutions suite extends into identity verification, fraud analytics, and regulatory compliance. The LSEG World-Check dataset, often used alongside LexisNexis products, covers 4.9 million profiles across 240+ countries.

Strengths: Unmatched data coverage for sanctions and PEP screening. Modular pricing allows institutions to buy specific capabilities without committing to a full platform. Strong presence in insurance, healthcare, and government sectors beyond traditional banking. Reliable screening accuracy with low miss rates on sanctions matches.

Limitations: Not a full AML platform in the modern sense. Transaction monitoring and case management require integration with third-party systems. The user experience reflects enterprise software design conventions rather than modern SaaS workflows. Data licensing costs can escalate significantly at scale.

Best fit: Multinational corporations and regulated entities that need best-in-class screening data and already have transaction monitoring infrastructure in place.

4. Hawk AI

Hawk AI takes a machine learning-first approach to transaction monitoring and screening. The platform uses supervised and unsupervised ML models to detect patterns that rules-based systems miss, while providing explainable outputs that compliance officers can audit and defend to regulators.

Strengths: Strong false positive reduction through ML model tuning, with some clients reporting 60-70% decreases in non-actionable alerts. Cloud-native architecture enables faster deployment than legacy competitors. The platform covers transaction monitoring, customer screening, and payment fraud in a unified interface. Good fit for institutions transitioning from rules-only systems to hybrid approaches.

Limitations: Smaller client base than established vendors means fewer reference cases in some verticals. The platform is still building out regulatory reporting capabilities for certain jurisdictions. Less depth in sanctions data compared to LexisNexis or ComplyAdvantage.

Best fit: Banks and payment providers looking to modernize transaction monitoring without a full rip-and-replace of existing infrastructure.

5. TRM Labs

TRM Labs specializes in blockchain intelligence. The platform maps cryptocurrency transactions across 30+ blockchains, identifies connections to sanctioned entities and illicit actors, and provides investigation tools used by both private institutions and government agencies including FinCEN and the IRS.

Strengths: Best-in-class blockchain analytics with cross-chain tracing capabilities. Real-time screening against OFAC and other sanctions lists for crypto addresses. Strong government and law enforcement relationships validate the underlying intelligence. The investigation workbench enables analysts to trace transaction flows visually.

Limitations: Focused exclusively on crypto and blockchain-related AML. Does not replace traditional fiat transaction monitoring. Pricing can be steep for smaller crypto exchanges. Limited value for institutions without crypto exposure.

Best fit: Crypto exchanges, DeFi protocols, banks with crypto custody offerings, and any institution that needs blockchain-specific AML coverage.

6. Alloy

Alloy positions itself as an identity decisioning platform rather than a pure AML tool. It orchestrates data from multiple sources, including credit bureaus, government databases, and watchlists, into automated decisioning workflows for onboarding, transaction monitoring, and ongoing due diligence.

Strengths: Flexible workflow builder allows compliance teams to create and modify rules without engineering support. Aggregates data from 190+ sources into a single decisioning layer. Strong KYC and KYB capabilities alongside AML screening. The no-code interface accelerates time to value for compliance teams.

Limitations: Transaction monitoring is less sophisticated than purpose-built AML platforms. The platform excels at onboarding and identity verification but has thinner capabilities for ongoing monitoring and SAR filing. Best suited to US-centric operations with more limited global coverage.

Best fit: US-based fintechs and banks that want to unify identity verification, KYC, and AML screening in a single orchestration layer.

How to Choose the Right AML Platform

Picking AML software is not a feature comparison exercise. It is an architectural decision that affects compliance operations for years. The right framework starts with four questions.

What is your primary compliance bottleneck?

If screening accuracy is the problem, platforms with strong proprietary data like ComplyAdvantage or LexisNexis will deliver the most impact. If alert volume from transaction monitoring is overwhelming your team, ML-driven platforms like Hawk AI or agentic approaches like Sphinx will matter more. If onboarding friction is the issue, Alloy's orchestration layer addresses that directly.

What does your existing infrastructure look like?

Institutions running core banking systems from Temenos or FIS may benefit from NICE Actimize's pre-built connectors. Cloud-native fintechs will get more value from API-first platforms. The integration cost often exceeds the licensing cost, so compatibility with existing data pipelines and case management systems should drive the decision.

How important is explainability?

FinCEN's 2026 proposed rule emphasizes effectiveness over volume, but regulators still expect institutions to explain their compliance decisions. Any AI-driven platform must produce audit trails that satisfy examiners. Black-box ML models that reduce false positives but cannot explain why they cleared an alert create a different kind of regulatory risk. Platforms like Sphinx address this through an interpretable agentic framework that logs every reasoning step.

What is your growth trajectory?

A platform that works for 1,000 daily alerts may collapse at 50,000. Cloud-native architectures scale more gracefully than on-premise deployments. But scale is not just about volume. It is about geographic expansion, new product lines, and evolving typologies. The platform must grow with the business without requiring a migration every two years.

Where Sphinx Fits

Sphinx approaches AML differently from every platform on this list. Rather than layering ML models on top of a traditional rules engine, Sphinx deploys autonomous AI agents that triage alerts the way a senior analyst would: gathering context, cross-referencing data sources, assessing risk, and documenting findings with full reasoning chains.

The result is a system that resolves risk alerts up to 99% faster than manual workflows. Each decision is logged with an auditable trail explaining what data the agent examined, what logic it applied, and what conclusion it reached. There is no black box. Every disposition can be reviewed, challenged, and defended to a regulator.

Sphinx does not replace transaction monitoring systems or screening engines. It operates downstream, taking the alerts those systems generate and automating the investigation and disposition work that currently consumes the majority of analyst time. For compliance teams drowning in alerts, that is where the leverage is: not in generating fewer alerts, but in resolving them faster without sacrificing quality or auditability.

Frequently Asked Questions

What is AML software and why do financial institutions need it?

AML software automates the detection, investigation, and reporting of potential money laundering and terrorist financing activity. Financial institutions are required by law, under the Bank Secrecy Act in the US, Money Laundering Regulations in the UK, and FATF standards globally, to maintain programs that identify and report suspicious activity. Without AML software, institutions would need to manually screen every customer and transaction against sanctions lists, monitor transaction patterns, and file regulatory reports. At the scale of modern financial services, that is not operationally feasible.

How much does AML software cost?

AML software pricing varies dramatically by vendor and buyer segment. Entry-level SaaS platforms like ComplyAdvantage start at approximately $99 per month for basic screening. Mid-market solutions typically run $50,000 to $250,000 annually depending on transaction volume and modules selected. Enterprise deployments from vendors like NICE Actimize or SAS can exceed $1 million annually including implementation, licensing, and ongoing support. Beyond licensing, institutions should budget for integration, data migration, training, and ongoing model tuning. Total cost of ownership over three years often runs 2-3 times the initial licensing quote.

What is the biggest problem with current AML software?

False positives. According to Facctum's 2026 compliance report, 85-95% of AML alerts are false positives, meaning they do not correspond to genuine financial crime risk. Compliance teams spend up to 90% of their time investigating alerts that lead nowhere. This creates analyst fatigue, delays the investigation of real threats, and drives compliance costs higher. The industry is now shifting toward AI-driven alert triage and agentic automation to address this problem at its root.

How is AI changing AML compliance?

AI is being applied at multiple layers of the AML stack. Machine learning models improve detection accuracy by identifying patterns that static rules miss. Natural language processing automates adverse media screening and document review. And agentic AI systems, a newer category, automate the full investigation workflow, from data gathering through risk assessment to disposition. Current data shows AI reduces false positives by up to 40%, and 62% of financial institutions already use some form of AI or ML in their AML monitoring. The shift is from AI as a detection enhancement to AI as an operational automation layer.

What should compliance teams look for when evaluating AML vendors?

Five criteria matter most. First, false positive reduction rates with evidence from comparable deployments. Second, explainability and audit trail quality, especially as regulators emphasize decision transparency. Third, integration complexity and time to value, since a platform that takes 18 months to deploy delays ROI by 18 months. Fourth, total cost of ownership including implementation, data, and ongoing support. Fifth, the vendor's regulatory coverage across the jurisdictions where the institution operates. Request reference calls with clients of similar size and complexity, and run a proof of concept on real production data before committing.

.png)