TL;DR: KYB (Know Your Business) is the due diligence process through which regulated institutions verify the identity, legitimacy, ownership structure, and risk profile of a business entity before establishing a commercial relationship. The global KYB market reached $3.7 billion in 2024 and is growing at over 18% annually, driven by beneficial ownership requirements now active in 170 countries. Getting KYB right determines whether an institution can onboard business customers at scale without regulatory exposure.

What KYB Actually Means

KYB — Know Your Business — is the verification process that determines whether a business entity is legitimate, who ultimately owns and controls it, and whether that entity poses unacceptable financial crime risk. Where KYC verifies individual identities, KYB addresses the structurally harder problem of verifying legal entities: companies, LLCs, partnerships, trusts, and other corporate structures where ownership can be layered, obscured, or deliberately hidden.

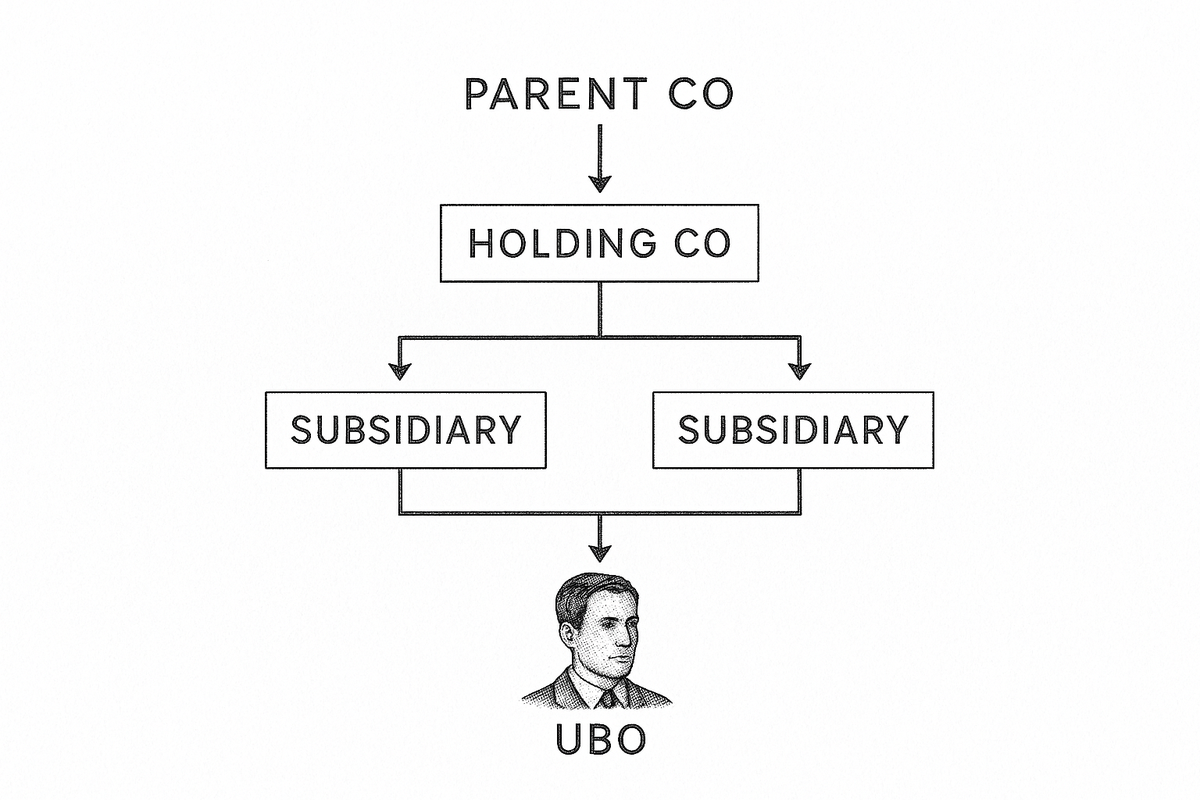

The complexity is architectural. An individual has one identity to verify. A business has a legal identity, a registration history, an ownership chain that may span multiple jurisdictions, and a set of ultimate beneficial owners (UBOs) who may sit behind several layers of holding companies. Each layer requires independent verification. Each jurisdiction has its own registry formats, data availability, and disclosure requirements. A KYB process that works for a Delaware LLC may fail entirely for a Cayman Islands SPV or a German GmbH with a Luxembourg parent.

For banks, fintechs, payment processors, and any institution that onboards business customers, KYB is not optional. It is a regulatory requirement under FinCEN's CDD Rule, FATF Recommendation 24, and the EU's Anti-Money Laundering Directives. The obligation is not merely to collect documents but to form a reasonable belief about who owns and controls the entity — and to maintain that understanding over time.

The Regulatory Backbone

Three overlapping frameworks drive KYB requirements globally.

FinCEN's Customer Due Diligence Rule has required covered financial institutions to identify and verify the beneficial owners of legal entity customers since May 2018. The rule defines beneficial ownership under two prongs: an ownership prong (any individual who directly or indirectly owns 25% or more of the equity) and a control prong (a single individual with significant responsibility to manage the entity). Institutions must collect name, date of birth, address, and identification number for each beneficial owner, and verify that information through documentary or non-documentary methods.

On February 13, 2026, FinCEN issued an exceptive relief order (FIN-2026-R001) that eased one element of this burden. Covered institutions no longer need to re-verify beneficial owners every time an existing legal entity customer opens a new account. Verification remains required at first account opening, when previously obtained information is called into question, and as risk-based monitoring otherwise demands. The beneficial ownership obligation at onboarding stands — the per-account repetition was relaxed.

FATF Recommendation 24, substantially revised in 2022, requires countries to ensure that adequate, accurate, and current beneficial ownership information on legal persons is obtainable by competent authorities without delay. The revision introduced a multi-mechanism model: countries must ensure verified ownership data is available from multiple overlapping sources, including company registries, regulated institutions, and the entities themselves. For banks and fintechs, this translates into concrete obligations ranging from collecting ownership declarations to cross-checking them against independent sources.

The Corporate Transparency Act added a federal beneficial ownership reporting requirement in the United States, though its scope has narrowed. A March 2025 interim final rule revised the definition of "reporting company" to apply only to foreign entities registered to do business in a US state. Domestic companies — and US persons who are beneficial owners — are now exempt from filing BOI reports with FinCEN. The CDD Rule's requirements for financial institutions remain intact regardless of these CTA changes.

In the EU, the Sixth Anti-Money Laundering Directive and proposed AML Regulation continue to strengthen beneficial ownership transparency requirements, with member states mandated to maintain central UBO registers accessible to obliged entities and competent authorities.

The net effect: a compliance team in 2026 faces beneficial ownership verification requirements from multiple regulatory bodies, each with slightly different thresholds, exemptions, and expectations. The KYB process must satisfy all applicable frameworks simultaneously.

What a KYB Process Covers

A complete KYB process moves through six stages, from basic entity validation through ongoing monitoring. Each stage addresses a distinct risk dimension.

Entity Identification and Verification

The process starts with confirming the business exists as a legal entity. This requires collecting the company's legal name, registration number, jurisdiction of incorporation, registered address, and legal structure (corporation, LLC, partnership, trust). That information is verified against official business registries in the entity's jurisdiction of incorporation.

Registry data quality varies dramatically by country. US state secretary of state databases are generally reliable for confirming active status but often lack ownership detail. UK Companies House provides structured ownership data. Many jurisdictions — particularly in the Caribbean, parts of Asia, and some Middle Eastern countries — maintain registries that are incomplete, outdated, or not publicly accessible.

Ownership Structure Mapping

Once the entity is confirmed, the next step is mapping its ownership chain. This means identifying all shareholders, parent companies, and holding structures between the entity and the individuals who ultimately own or control it. For simple structures — a single founder owning 100% of an LLC — this is straightforward. For multi-layered corporate structures with entities across jurisdictions, it requires tracing ownership through each intermediate holding company until reaching natural persons.

Ownership mapping is where many KYB programs break down. Complex structures can involve circular ownership, nominee shareholders, bearer shares (still legal in some jurisdictions), trusts with discretionary beneficiaries, and partnerships where control and economic interest diverge. Each of these requires a different analytical approach and often manual investigation.

Beneficial Owner Verification

pWith the ownership structure mapped, the institution must identify and verify every UBO who meets the applicable threshold. Under FinCEN's CDD Rule, that means any individual owning 25% or more of the equity and at least one individual exercising significant control. FATF Recommendation 24 does not prescribe a single threshold, and some jurisdictions have adopted lower ones — the EU uses 25% as a default but member states can go lower.

For each identified UBO, verification follows a process similar to individual KYC: collecting name, date of birth, address, and government-issued identification, then verifying that information through documents or non-documentary methods such as credit bureau data or public records. The institution must form a reasonable belief that it knows the true identity of each beneficial owner — not merely that paperwork has been filed.

Sanctions, PEP, and Adverse Media Screening

Both the entity and its beneficial owners must be screened against sanctions lists (OFAC SDN, UN, EU, UK), politically exposed persons databases, and adverse media sources. Screening applies at onboarding and must be repeated as watchlists update. A sanctions match on any beneficial owner is a match on the business relationship.

This is where false positive rates become operationally significant. Name-matching algorithms applied across multiple jurisdictions, transliterated names, and common surnames generate substantial alert volumes. Teams that lack automated screening triage spend disproportionate analyst time clearing matches that are obviously not true hits. Solutions that incorporate contextual matching — date of birth, jurisdiction, entity type — into the screening logic reduce false positives without sacrificing coverage.

Risk Assessment

Verified information feeds into an overall risk score for the business relationship. Risk assessment considers multiple dimensions: the entity's industry and jurisdiction, the complexity of its ownership structure, PEP or adverse media exposure of its principals, the nature and expected volume of transactions, and any other factors the institution's risk appetite framework considers material.

Higher-risk entities trigger Enhanced Due Diligence — deeper investigation into the source of funds, source of wealth, business model viability, and any other factors needed to form comfort with the relationship. The risk assessment is not a one-time score but a baseline that informs the intensity and frequency of ongoing monitoring.

Ongoing Monitoring

KYB does not end at onboarding. Institutions must monitor for changes in ownership, corporate structure, sanctions status, and risk profile throughout the relationship. Periodic reviews — annual for standard risk, quarterly or more frequently for elevated risk — confirm that previously verified information remains accurate.

Trigger-based monitoring supplements periodic reviews. Changes in transaction patterns, adverse media hits, sanctions list updates, or corporate registry filings can trigger re-verification outside the scheduled review cycle. FinCEN's 2026 exceptive relief order reinforced that institutions need not re-verify at every account opening, but must still maintain procedures to detect and respond to material changes.

KYB vs KYC: Why Business Verification Is Harder

KYC and KYB share a common purpose — knowing who you are doing business with — but diverge in structural complexity.

An individual KYC check verifies one person's identity against one set of documents. The data sources are standardized: government-issued ID, proof of address, possibly a credit bureau check. The person either is who they claim to be, or they are not.

KYB multiplies this problem. A single business entity can have dozens of shareholders across multiple jurisdictions, each requiring individual verification. The ownership structure itself must be mapped — a task that requires understanding corporate law across every jurisdiction in the chain. And unlike individual identity, corporate ownership changes: shareholders sell stakes, new investors come in, parent companies restructure. An accurate ownership picture at onboarding can become stale within months.

The data infrastructure differs too. Individual identity verification benefits from mature credit bureau databases, standardized government ID formats, and biometric matching. Business verification relies on corporate registries that vary in quality, availability, and format from country to country. There is no global equivalent of a passport number for businesses.

According to a Juniper Research report, total global KYC and KYB spend will reach $35.5 billion in 2026 and grow to $53 billion by 2030. A significant share of that spend still goes toward manual processes that automation has not yet reliably replaced — particularly in ownership structure mapping and cross-jurisdictional UBO verification.

How to Evaluate KYB Solutions

Five capabilities separate effective KYB platforms from those that create more work than they eliminate.

Registry coverage and data quality. The foundation of any KYB solution is its ability to access and normalize business registry data. Ask how many jurisdictions the vendor covers, whether data is pulled in real time or from periodic snapshots, and how the system handles registries that lack structured ownership data. Coverage claims without data quality are misleading — accessing a registry that has not been updated in two years provides false comfort.

Ownership structure resolution. The system should trace ownership through multiple layers of corporate entities automatically, flagging circular ownership, nominee structures, and gaps in the chain. Manual ownership mapping does not scale. Ask how the system handles multi-jurisdictional chains and what happens when a link in the chain cannot be automatically resolved.

Screening integration and false positive management. Sanctions, PEP, and adverse media screening must apply to both the entity and its beneficial owners, with ongoing re-screening as watchlists update. Equally important is how the system handles false positives. Name-matching across transliterated names and common surnames generates noise. Contextual matching — incorporating date of birth, jurisdiction, and entity type into the matching logic — saves meaningful analyst time.

Risk-based workflow automation. Not every business entity requires the same level of diligence. Low-risk entities with simple ownership structures in well-regulated jurisdictions should move through onboarding quickly. Complex, high-risk entities should route to senior analysts with the right context already assembled. Ask whether the system supports configurable risk scoring and automated routing, and how it handles industry-specific risk frameworks like those required for crypto businesses.

Ongoing monitoring and trigger management. A KYB solution that only works at onboarding creates a verification cliff — accurate at day one, degrading from day two. Evaluate how the system monitors for corporate registry changes, sanctions list updates, and adverse media throughout the relationship lifecycle. Ask what triggers re-verification and how alerts from ongoing monitoring are routed and resolved.

The KYB market reached $3.7 billion in 2024 and is growing at over 18% annually, according to Dataintelo. That growth reflects a market moving from manual, document-driven verification toward automated, API-integrated platforms. But automation quality varies enormously. The right question is not whether a vendor offers automation, but what happens when automation reaches its limits — how the system handles the cases that cannot be resolved without human judgment.

Where Sphinx Fits

Sphinx operates at the investigation and remediation layer of KYB workflows, automating the analyst work that follows initial verification: screening alert triage, UBO documentation review, case summarization, and audit trail generation. Sphinx's agents work inside existing compliance platforms — reviewing the same data analysts would review, logging every decision through the Interpretable Agentic Framework, and routing complex cases to human reviewers with full context already assembled.

For teams handling high volumes of business onboarding, the bottleneck is rarely the initial data collection — it is the analyst capacity to review, verify, and disposition the results. Sphinx addresses that bottleneck directly, clearing screening queues and reducing case review time by up to 80% while maintaining a defensible audit trail for every decision.

Frequently Asked Questions

What is the difference between KYB and KYC?

KYC (Know Your Customer) verifies the identity of individual persons. KYB (Know Your Business) verifies legal entities — companies, LLCs, partnerships, and trusts — including their ownership structures and the individuals who ultimately control them. KYB is structurally more complex because it requires tracing ownership through potentially multiple layers of corporate entities across different jurisdictions.

Who is required to perform KYB?

Banks, credit unions, money services businesses, broker-dealers, and other financial institutions covered by FinCEN's CDD Rule must identify and verify beneficial owners of legal entity customers. Fintechs and payment processors operating under banking partnerships or their own licenses carry the same obligations. Non-financial businesses may face KYB requirements under specific industry regulations or as part of B2B due diligence.

What is a beneficial owner under FinCEN's CDD Rule?

FinCEN defines a beneficial owner under two prongs: any individual who directly or indirectly owns 25% or more of the equity interests of the legal entity (ownership prong), and a single individual with significant responsibility to control, manage, or direct the entity (control prong). At minimum, one person must be identified under the control prong.

How often must KYB verification be updated?

There is no single mandated frequency. FinCEN's 2026 exceptive relief order clarified that re-verification at every new account opening is no longer required. Institutions must maintain risk-based ongoing monitoring programs that trigger re-verification when ownership changes, adverse information surfaces, or periodic reviews indicate previously obtained information may be inaccurate. Higher-risk relationships warrant more frequent review cycles.

Can KYB be fully automated?

Straightforward entities with simple ownership structures in well-regulated jurisdictions can be verified largely through automated registry checks and screening. Complex structures — multi-layered holding companies, entities in jurisdictions with limited registry data, nominee shareholders, or trusts with discretionary beneficiaries — still require human judgment at critical points. The most effective KYB programs automate what can be automated and route the rest to analysts with the right context already assembled.

.png)