TL;DR: Compliance costs in fintech consume 10-20% of operating expenses and rise faster than revenue at most growth-stage companies. The standard response is to hire more analysts and buy more tools. Both scale linearly while the underlying problem compounds. The fintechs actually bending their cost curve are automating case-level work — replacing the repetitive alert triage that accounts for 80% of compliance labor — not cutting corners on coverage.

The Cost Problem Nobody Models Correctly

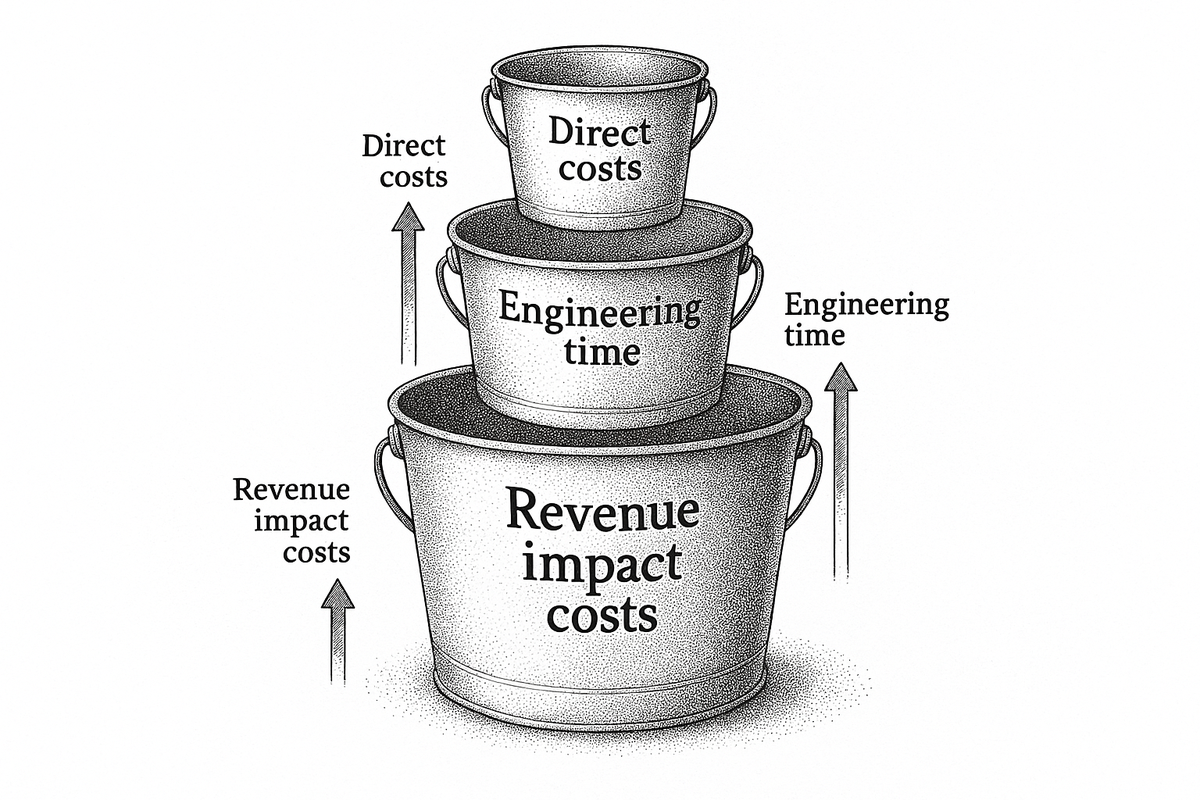

Ask a fintech CFO what compliance costs and you will get a number covering software licenses, audit fees, and headcount. That number is wrong — not because it is fabricated, but because it only captures direct spend.

The real cost includes three buckets most fintechs only model one of. Direct costs — legal counsel, AML/KYC vendors, SOC 2 audits, sanctions screening — are the visible line items. A 2026 FintechSpecs analysis puts these at $75,000-$250,000 at seed stage, climbing to $300,000-$700,000 by Series A. According to Culta's 2026 fintech benchmarks, compliance consumes 10-20% of operating expenses across the sector, with neobanks at 18-22%.

But direct costs are the smallest bucket. Engineering time — weeks per quarter your developers spend on compliance integrations, audit trail infrastructure, and onboarding rework — often exceeds the dollar value of your compliance tooling. Revenue impact costs — onboarding friction that kills conversion, feature delays while reviews pile up — are larger still. Most fintechs never model these. They are surprised by their burn rate, and the surprise is self-inflicted.

We see this repeatedly. A fintech will cite a compliance budget of $400,000. When we walk through analyst hours on false positives, engineering sprints consumed by audit preparation, and onboarding drop-off from manual review bottlenecks, the real number is closer to $1.2 million.

Why Hiring More Analysts Does Not Scale

The default response to rising compliance costs is to hire. Alert volumes growing — add analysts. Regulatory scope expanding — add specialists. AML backlog six months deep — post three roles and hope the recruiter delivers before the next examination.

This has a structural problem. Compliance headcount scales linearly while workload compounds. Transaction volumes grow with the business. Each new jurisdiction adds requirements. Each regulatory update — FinCEN's April 2026 proposed AML/CFT reform is the latest — layers obligations onto an already stretched team. You cannot hire your way out of a compounding problem with a linear resource.

The numbers confirm this. Mid-market banks spend $8-20 million annually on compliance personnel alone — 80-150 staff at fully loaded costs of $95,000-$135,000 each. Fintechs face the same per-analyst cost without the revenue base to absorb it.

Worse, a third of financial services professionals plan to leave the industry due to high-pressure workloads. Each departure triggers recruitment that costs months and produces a replacement who needs six more months to reach productivity. The cost of compliance is not just what you pay your team. It is what you pay to replace them.

The Shift: From Headcount to Case Automation

The fintechs reducing compliance costs are not loosening thresholds or skipping steps. They are automating the work itself — the repetitive case review that consumes 80% of analyst time but requires only 20% of their expertise.

Most compliance technology automates detection — faster alerts, more screening lists, broader monitoring. But detection is not where the cost sits. The cost sits in what happens after the alert fires: an analyst opens the case, pulls transaction history, checks sanctions databases, reviews customer profiles, writes disposition notes. That takes 30-45 minutes per alert. With 85-95% being false positives, the vast majority of that labor produces no actionable outcome.

Case-level automation replaces the labor, not the judgment. AI agents that review data, cross-reference entities, apply institutional policies, and produce audit-ready documentation transform compliance from a headcount-dependent function to a technology-leveraged one. Across our customer base, institutions deploying case-level AI see 80-87% of routine cases resolved without human intervention — freeing analysts for the complex investigations regulators actually want humans making.

Four Levers That Bend the Cost Curve

Cost reduction in compliance is a design discipline. The fintechs bending their cost curves pull four levers simultaneously.

Automate case-level investigation. Each false positive costs $25-50 in analyst time. A program generating 100,000 alerts annually spends roughly $4.75 million investigating noise. Cutting that by 80% through AI triage transforms compliance from a function that scales with headcount to one that scales with technology.

Fix false positive rates at the source. Legacy rule-based monitoring produces false positive rates of 90-99%. Better data foundations, contextual detection, and entity resolution drop that rate before alerts reach an analyst. But tuning without governance documentation creates regulatory risk — the fix must be auditable and defensible.

Embed compliance into the product layer. Compliance-as-code — encoding policies, risk ratings, and controls as testable definitions — eliminates the sequential build-review-rebuild cycle. Fintechs treating regulatory requirements as design constraints compress review cycles from weeks to hours.

Automate audit trail generation. Audit preparation is one of the largest hidden costs. Teams generating structured, timestamped evidence as a byproduct of normal operations eliminate a cost center that grows with every regulatory cycle.

The Regulatory Tailwind

For the first time, the regulatory environment is aligned with cost reduction.

FinCEN's April 2026 proposed rule refocuses AML/CFT obligations on effectiveness rather than procedural volume, explicitly allowing institutions to direct resources away from lower-risk areas. The rules aim to "reduce unnecessary compliance burdens" while concentrating resources on higher-risk activities. This is not deregulation — it is a recalibration that rewards programs demonstrating risk-based allocation over programs processing high volumes of low-quality alerts.

The EU is moving similarly. DORA implementation costs have hit 2-5 million euros for most institutions. The ones absorbing these costs efficiently have automated evidence generation and risk-based monitoring — not the largest compliance teams.

For fintechs, this shift creates an advantage. You can build compliance architecture from scratch with automation-first design. Incumbent banks are retrofitting legacy processes. The cost of building it right the first time is a fraction of fixing it later.

Frequently Asked Questions

How much do fintechs typically spend on compliance?

Seed-stage fintechs spend $75,000-$250,000 annually on direct compliance costs. Series A companies budget $300,000-$700,000. Growth-stage fintechs routinely spend $500,000 to $1.8 million per year on direct costs alone, excluding engineering time and revenue impact. Compliance typically consumes 10-20% of fintech operating expenses.

What is the biggest compliance cost driver for fintechs?

Personnel, accounting for 50-65% of total compliance spend. Fully loaded analyst costs run $95,000-$135,000 per person. The compounding factor is that headcount needs grow with transaction volume, but each hire adds the same fixed cost regardless of incremental risk addressed.

Can fintechs reduce compliance costs without increasing regulatory risk?

Yes, by reducing labor costs through automation rather than reducing coverage. Case-level AI removes the repetitive work accounting for 80% of analyst time while maintaining audit readiness. FinCEN's 2026 reforms explicitly support risk-based resource allocation.

How does compliance-as-code reduce costs?

It encodes regulatory requirements as testable definitions within engineering workflows, eliminating the build-review-rebuild cycle that adds weeks to product launches. Violations are caught before reaching a human reviewer, reducing remediation costs and the compliance team's review burden.

What ROI should fintechs expect from compliance automation?

Institutions deploying AI case-level automation see 80-87% of routine cases resolved without human intervention. At $25-50 per alert, a program processing 100,000 alerts annually can reduce investigation costs by $3-4 million, plus savings from reduced hiring, faster onboarding, and lower attrition.

.png)